The UK government is spending an enormous amount on COVID-19 – supporting the health service, helping to relieve the suffering of those who have lost their incomes, and helping businesses keep afloat.

This spending policy has now been endorsed by the International Monetary Fund. Governments of advanced economies should spend more, says the IMF, not just to keep their economies in good shape until the pandemic passes, but also to invest in preparation for a post-COVID recovery.

And we should not worry that all this extra spending is causing a big rise in government debt. Although the UK debt/GDP ratio has already risen above 100%, the government should spend even more. This will stimulate GDP growth and thus stabilise debt/GDP.

The way to cope with high government debts, the IMF says, is no longer austerity – higher tax and lower spending – but rather the opposite, at least while the pandemic is with us.

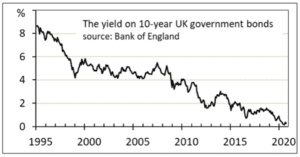

A vital ingredient for the success of this high-spend policy is low interest rates. The UK government’s cost of new borrowing for 10 years is currently 0.3%; it has never been so cheap. The Bank of England is playing an important part in keeping it that way.

How are we paying for it?

To pay for all the extra spending, the government is borrowing in the usual way from the private sector – from pension funds and insurance companies, for instance. It does this by selling bonds, which are promises to pay back with interest. In the period April 2020 to June 2020 it borrowed an extra £150bn. Yet, as fast as the government is selling bonds, the Bank of England is buying them from their private sector holders – paying with newly created money. Technically, this money is “reserve” deposits, which are claims against the Bank of England itself.

Indirectly the Bank of England is therefore financing much of the government’s new spending. And, crucially, its continuing demand for government debt is holding down the interest rate that the government has to pay to borrow.

The Bank of England insists that this massive quantitative easing (QE) programme of bond-buying is not driven by a need to support government finances. Rather, the motive is to fulfil its mandate to control inflation, which has been falling increasingly below the 2% target for over a year. The government’s need for finance and the Bank of England’s bond purchases are both consequences of the recessionary conditions, and it is a coincidence that its purchases of bonds and the government’s sales have been at similar rates.

You might think that this is splitting hairs, but it matters. If the government can rely on the Bank of England to buy its bonds as necessary to prevent interest rates from rising, then it is hard to be confident that the bank will raise rates enough when needed to stop inflation rising.

And the current low-inflation environment may be short lived.

Inflation may rise

Consumer spending has fallen markedly during 2020. Among the causes, restrictions on several sectors of the economy, notably tourism and leisure, have forced people to save rather than spend. When the restrictions are relaxed, pent-up demand may lead to rising prices, especially if the supply of goods and services is reduced because some businesses have not survived.

On the other hand, some argue that rising unemployment will hold down wages and hence prices, and others expect the recovery to be gradual, giving time for supply to adjust. Moreover, with consumption patterns changing, price changes will vary across sectors, leading to doubt about the overall effect on inflation.

A deeper reason to expect inflation has been proposed in a new book by economists Charles Goodhart and Manoj Pradhan. They argue that the current low-interest rate, low-inflation conditions are associated with a favourable dependency ratio. This measures the numbers of young and old people (0 to 14 and over 65 years of age) relative to those in between who are presumed to be the working population. For the last three decades we have been in a “sweet spot”, they say, with plenty of workers globally to support the non-workers. This has held down wages and led to high saving which, in turn, has contributed to the long-term decline in interest rates.

But the age composition of populations is changing. With people living longer and birth rates declining, the dependency ratio is rising. There are fewer workers and more people who depend on their output; moreover, the old are requiring increasing care. To balance supply and demand, wages and prices must rise.

If inflation starts rising, the Bank of England’s response should be to choke off demand by raising interest rates. However, this will dampen economic growth, which may still be fragile. It will depress the price of assets, including property, and it will make debts more expensive to service, including public and private sector debts, both of which have been elevated by the pandemic. Under the IMF’s projected increase in government debt to 117% of GDP, even a small increase in rates would make this debt significantly harder to sustain.

While the Bank of England is adamant that it will not divert its attention from the 2% inflation target, other central banks are more equivocal. In the United States for example, Jay Powell, the chairman of the Federal Reserve Board, which sets monetary policy, has recently announced that future US inflation will be allowed to exceed its target for a period of time before monetary policy is tightened.

Despite the Bank of England’s insistence, its accommodating behaviour during the Covid crisis suggests that it, too, may take a more flexible attitude towards future inflation.

This article was originally published on The Conversation.

John Whittaker is Senior Teaching Fellow in Economics at Lancaster University.