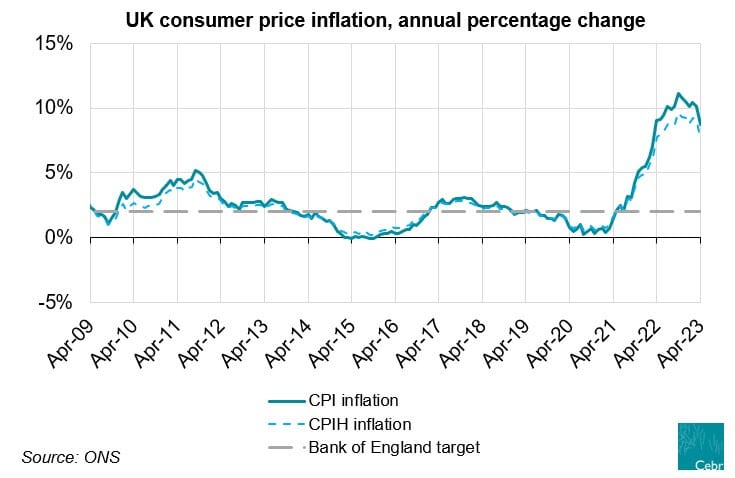

UK inflation on the Consumer Prices Index (CPI) measure slowed to 8.7% in April, according to data released by the Office for National Statistics (ONS) this morning in line with Cebr’s forecast for the month. The rate of price growth on the CPI measure has now fallen below 10% for the first time since August 2022. Core inflation, which excludes volatile consumption categories such as food and energy, accelerated to 6.8% in April, having stood at 6.2% in March. Other measures of inflation, such as the Consumer Prices Index including owner occupiers’ housing costs (CPIH) and Retail Price Index (RPI), also decelerated sharply in April.

April marked a second consecutive month of deceleration in the CPI inflation rate. Indeed, at a decline of 1.4 percentage points, this was the largest monthly fall in the inflation rate in over 30 years. Amongst the main inflation categories, housing and household services was the main contributor to the monthly decline in the inflation rate, with price growth in April slowing to 12.3%, down from 26.1% in March. Within this category, particularly stark slowdowns in price growth were witnessed for electricity and gas. In the case of the former, price growth in April amounted to 17.3%, having stood at as high as 66.7% in March. Meanwhile, for the latter, price growth of 36.2% was witnessed in April, down from 129.4% in March. These sharp month-on-month slowdowns largely reflect a base effect from April 2022, which saw a large uplift to the Ofgem price cap and considerable upward pressure on household energy bills. However, there are nearer-term factors to consider, including recent falls in wholesale energy prices, which have contributed to slight month-on-month declines in energy prices for consumers. For instance, gas prices faced by consumers fell by 1.0% between March and April this year. Based on the trends in wholesale prices, we expect further sharp declines in energy price inflation from July onwards.

Several consumption categories saw an acceleration in their respective rates of inflation between March and April. This partially offset the impact of the energy price growth slowdown on the headline rate of inflation. For instance, the alcohol and tobacco category saw annual inflation of 9.1% in April, up from 5.3% in March, while price growth in communication was 7.9% in April, up by 4.2 percentage points on March’s value. Continued acceleration of price growth across non-energy consumption categories will be cause for concern, as it provides evidence that inflation is becoming more deeply embedded across the wider economy. This is further highlighted by the acceleration of the core CPI rate in April. At 6.8%, this represented the fastest rate of core inflation since March 1992 and increases the likelihood of a further 25 basis point interest rate hike by the Bank of England next month. Price growth for another key consumption category, food and non-alcoholic beverages, remained high in April, at 19.0%. This was slightly down on March’s reading of 19.1%, however.

Cebr forecasts inflation to continue its decelerating trend for much of the year, driven by the base effects from 2022’s energy price volatility and further falls in wholesale energy prices. However, we expect elevated inflation to linger for an extended period. For instance, by December 2023, we still anticipate inflation to be around 4.0%, standing at twice the Bank of England’s target rate. Though we expect many consumption categories to exhibit decelerating inflation over 2023, some are expected to be stickier than others. Food and non-alcoholic beverages inflation is forecasted to remain above the headline CPI for the rest of the year, for instance, with this also being the case for hotels, cafes, and restaurants.

Sam Miley is a Senior Economist at the Centre for Economics and Business Research